Remember that heart-stopping moment when people started posting about their lost GCash money?

It was Saturday morning; we were driving across Batangas from a very fun vacation when we received a text from Gcash about an unauthorized transaction.

I casually opened my partner’s Gcash account and saw four (4) Send Money transactions in ₱2,000 increments.

It’s impossible that either of us has clicked on phishing links, as we’re very cautious about these matters because we both worked in a fraud department of an international bank.

While my heart stopped because ₱8,000 is still ₱8,000 and that could’ve been spent on other important things, I tried to be calm and reported the unauthorized transaction.

I know the lost money would be back because it was clearly a glitch. We knew it was a glitch because one, Gcash texted us the unathorized transaction (it’s not like we saw the lost money and notified Gcash, but the other way around which means they knew about it); and two, we know how the process works in fraud claims.

When I opened our social media accounts, suddenly, group chats were buzzing with “HOY CHECK YOUR GCASH!” and Facebook turned into a virtual panic room.

While GCash eventually fixed the issue and returned the money, let’s be honest—those few hours of uncertainty had us all thinking, “Should I really keep all my money in one e-wallet?”

What if we need to make an urgent payment during these technical hiccups? Or worse, what if we’re stuck with zero access to our funds when we need them the most?

Being dependent on just one E-wallet is risky. While most establishments accept Gcash, even tricycles and sari-sari stores, it’s crucial to have backup options.

I just want to remind you that no e-wallet is safe from technical glitches, may it be Gcash or Maya, they are all prone to technical issues, and that’s just a fact.

But if you want to check on your options, here are five other e-wallets you want to download on your phone and put your money in (some have great interest rates).

1. Maya (formerly PayMaya)

Aside from Gcash, Maya is one of the famous OG Digital Wallets in the Philippines. Almost everyone has Gcash and Maya, but what makes it better than GCash?

My favorite Maya tool is their Personal Goals. It really helped me reach my target savings for the downpayment of our house and car. It helped me organize my money too, all this while earning 4% on the personal goals.

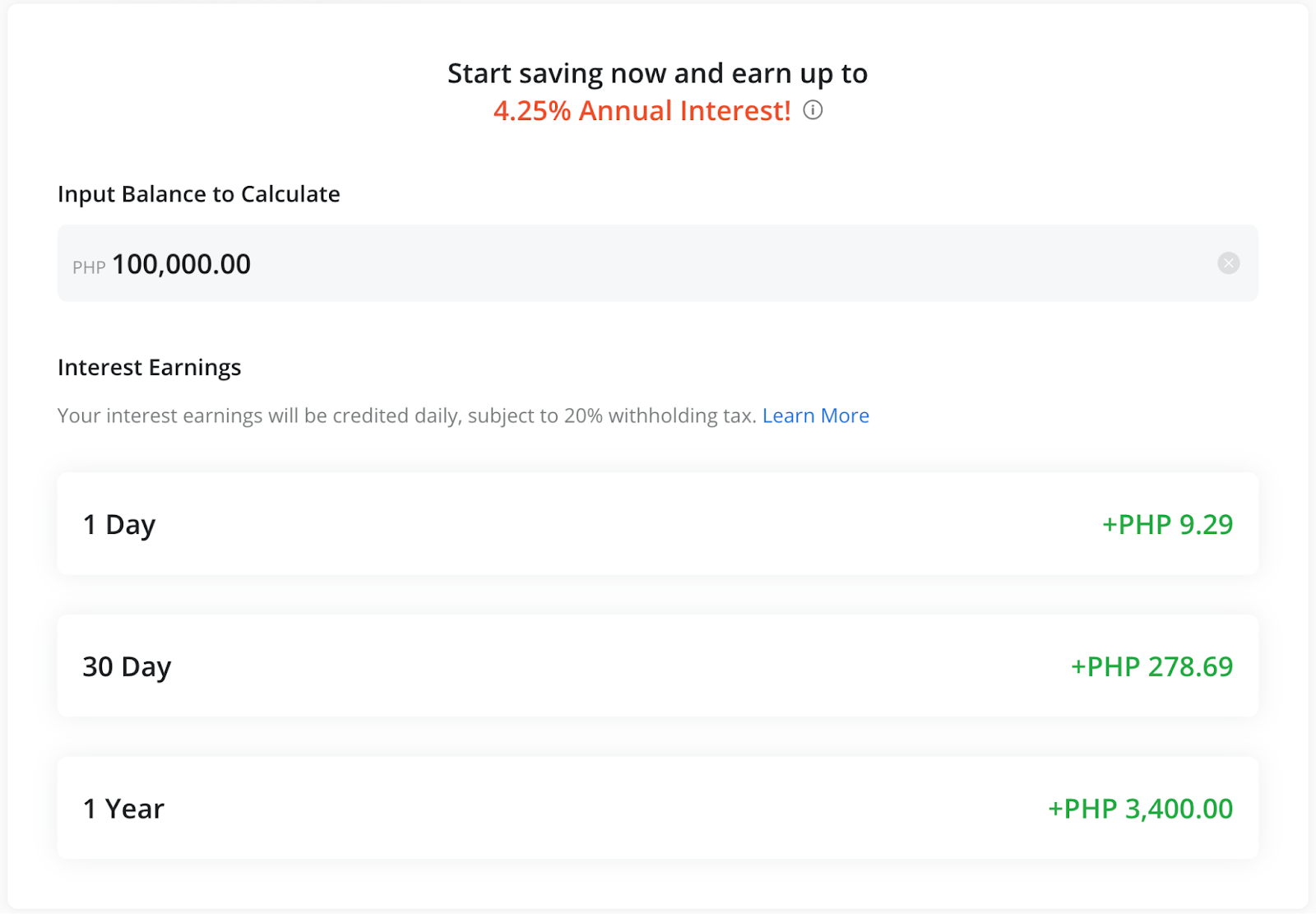

- Maya offers 3.5% interest rates per annum but you can get up to 15% interest boost on savings as long as you complete the “missions”

- You can get your own personalized physical card with your username printed on it

- If you’re into crypto, Maya has that option too, as well as time-deposit

- Compared to other digital banks, the interest rate in Maya is credited daily.

- Cashback promotions are also available on Maya

- If you love Landers, you can apply for the Landers Cashback Credit that is powered by Maya (just be responsible on your credit card bills especially if you’re a beginner.

Credit Card Guide for Beginners

2. GoTyme

GoTyme is the new kid on the block. Established in 2022, GoTyme is rising, and a lot of people have been signing up.

I opened my GoTyme account with the help of a bank ambassador while doing my grocery shopping at Shopwise, and I got my personalized Visa debit card on the spot. it took me less than five minutes to set everything up.

I then linked my Robinsons Rewards Card, so I can manage both accounts in one app.

You can open your GoTyme account at kiosks on Robinson’s retail outlets, or you can also download the GoTyme App.

- GoTyme offers a savings account with an interest rate of 4% per annum

- You can earn up to 3x Rewards Points if paying using your GoTyme Visa Card at Robinsons stores

- 3x free bank transfers given per week

3. Seabank

Another new kid on the block, created by the company behind Shopee. I opened my SeaBank account because the interest rates are so attractive!

Compared to Maya where you have to do your “missions” in order to get higher interest rates, Seabank offers 4.25% interest rate at the moment, without any missions whatsoever.

It’s also very easy to open a SeaBank account; all you need is your government ID, fill in some of your personal information, and that’s it. And the best thing about it is you can get even more discounts on your Shopee purchases when you pay using your SeaBank account.

- Discount on loads when buying straight from the app

- You can add a reminder for your monthly bills so you won’t miss your due date

- Free Transfers weekly to other banks and e-wallets for free using services like InstaPay and PESONet, with up to 15 free transfers weekly

- Seabank needs multiple authentications to transfer money or make payments, compared to other competitors where you can just send money easily without further verifications, making it easier for scammers or thieves to get your funds.

- Deposits in Seabank are also insured by the Philippine Deposit Insurance Corporation (PDIC) for up to PHP 500,000 per depositor, providing peace of mind regarding fund safety.

4. GrabPay

If you love using GrabCar, GrabFood and other Grab services, then GrabPay is the e-wallet for you.

I like how you can cash-in with your Grab driver when you’re on the go, which makes it very convenient.

Aside from the easy cashless payments for Grab services, there are also other benefits in opening a GrabPay account.

- You can earn an extra 50% points every time you use GrabPay to pay for your rides, food orders, and deliveries.

- You can also earn rewards when using GrabPay for paying in retail stores, as they are widely accepted too.

- You can cash-in using your HSBC Visa Card without any additional cost

5. CIMB

CIMB, the bank behind GSave, is one of the OG E-wallets in the Philippines. While your Gcash money is not insured, your money on GSave under CIMB is insured by PDIC.

If you had GCredit before, then you know how they can be annoying when you’re a day late on your loan, but they were the first e-wallet banks who offered online credit (very high interest rates, so we don’t suggest it).

- Savings interest rates are at 2.5% per annum which is not as high as their competitors

- They provide free life insurance up to ₱250,000 as long as you have ₱5,000 in your GSave account. The amount will be based on your average daily balance or ADB.

Remember: These banks and e-wallets often update their rates and promos, so follow their social media pages for the latest deals.

Let’s be real, that scary GCash glitch last week taught us all a valuable lesson – convenience shouldn’t compromise security. Call me paranoid, but spreading my money across different e-wallet platforms makes me feel more secure, and I guess, practical.

While GCash isn’t going anywhere (let’s face it, it’s still going to be a staple in our phones), spreading our financial eggs across different digital baskets isn’t just smart—it’s necessary.

Comments